Introduction

This article is inspired by a recent discussion on the “CDR Policy Scoop” podcast co-hosted by Sebastian Manhart and Eve Tamme, titled “Corresponding Adjustments: Necessary or Overkill” which was an inspiring debate as part of the Showdown series. It was about whether voluntary offsetting should require Corresponding Adjustments (CAs). Olga Gassan‑zade, former chair of the Paris Agreement’s Article 6.4 Supervisory Body and leading expert on carbon markets and international climate policy, argued that CAs are needed to avoid double counting and align the VCM with the Paris Agreement. Johan Börje from Stockholm Exergi, explained why finance stacking without Corresponding Adjustments is essential right now.

This was an argument I found very interesting when I first encountered it at COP29 in Baku, during a panel at the Sweden pavilion, challenging the standard narrative around carbon accounting, that CAs are not necessary for durable CDR between companies and countries. Which I agreed to. And I enjoyed listening to the recent podcast about it, I agreed it once again.

The debate often focuses on a fear of double counting. I kept asking myself if CAs are truly necessary for integrity, while creating a bureaucratic bottleneck for durable CDR. I believe we need to move away from treating the Voluntary Carbon Market (VCM) as an “external” trade. Instead, we can see it as a Nested System. This approach recognizes physical reality without stopping the early-stage capital that durable CDR projects need right now. And it is based on a systemic perspective.

The Logic of Nested Accounting: A Systemic Perspective

CAs may act as a barrier for durable carbon removals among companies and countries that remain within national borders. The reasoning for this does not seem to be a functional requirement for future removals, rather a reaction to past mistakes and failures of an emerging system. To scale durable CDR, we better acknowledge that public-private partnerships are essential to overcome initial deployment challenges.

The Industrial Precedent We can look at how we already account for green steel or renewable energy, as highlighted by Johan Börje at the Showdown podcast. When a government provides aid or creates a favorable regulatory environment for a green steel factory, the resulting emission reductions are naturally aggregated into the host country’s NDC. Simultaneously, the factory claims those reductions against its own corporate goals. We do not call this “double counting” for steel, and yet it is discussed as “double counting” for durable CDR.

Territorial Reality vs. Corporate Claims A country’s inventory is a map of physical reality. If a ton of carbon is removed within its borders, the national math must reflect that to stay accurate. Ignoring these removals because of private funding creates “ghost tons“* leading to a distorted view of global progress. At the same time, companies require a clear claim to justify the high cost of durable removals to their shareholders.

The Systemic Justification This is a systemic perspective because it treats climate accounting as a hierarchy of responsibility rather than a zero-sum trade. It treats the climate as a singular, interconnected system where different actors (nations vs. corporations) operate at different scopes. Nations are responsible for official territorial outcomes, corporations are responsible for their own targets and value-chain impacts. As long as national and corporate ledgers are never aggregated into a single global total, there is no mathematical “double counting.” They exist in harmony as nested layers of data.

The Precedent: Moving from Fragmented to Nested Systems

The logic of a Nested System is not a theoretical novelty; it has been operationally mapped for over a decade within the framework of REDD+ (Reducing Emissions from Deforestation and Forest Degradation). The World Bank’s 2021 “Nesting of REDD+ Initiatives: Manual for Policymakers“, commissioned by the Forest Carbon Partnership Facility (FCPF) and prepared by experts from Climate Focus and the World Bank, provides a detailed blueprint for integrating project-level activities into national-scale commitments. The core objective of nesting in that context is identical to the challenge we face today in scaling durable CDR: aligning the accounting of greenhouse gas removals across multiple scales.

Lessons from the Past When we look at the historical friction in REDD+ nesting, it is clear that the issues did not arise from the logic of “co-claiming” or the nesting architecture itself. Instead, the problems occurred because the institutional and digital systems were not developed for interoperability. As the Planning Guide: Integrating REDD+ accounting within a nested approach (2016) by Climate Focus highlights, the primary bottlenecks were administrative fragmentation and the lack of an accounting hierarchy. Projects were treated as isolated islands rather than functional units within a national whole. The failure wasn’t that the country and company both “counted” the impact; the failure was that the systems couldn’t talk to each other to ensure those counts stayed in their respective lanes.

Digital Interoperability as the Solution The failure of early systems was a failure of execution, not principle. Recent research, such as the policy brief article “Nested Climate Accounting for Our Atmospheric Commons,” published at Frontiers (2021) argues that we now have the digital tools; specifically distributed ledger technologies to solve these fragmentation issues. This allows for “trusted interoperability,” where data flows seamlessly from a project site to a national ledger. This technical architecture ensures that every removal is visible, preventing the creation of “ghost tons”; real atmospheric progress that exists in physical reality but is missing from the official national ledger.

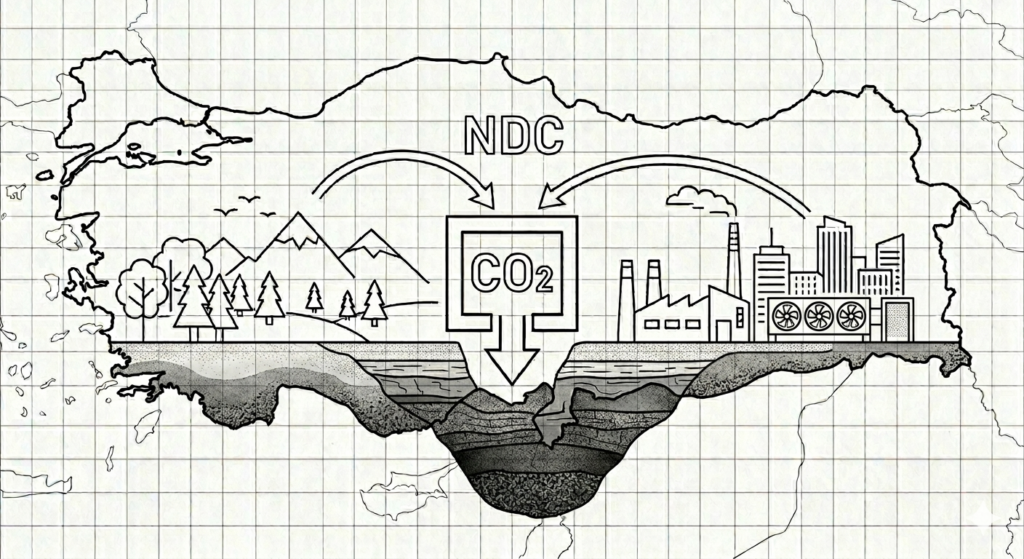

Two Ledgers, Different Scopes A nested approach acknowledges that a country and a company operate on two different layers of responsibility.

- The National Inventory (the NDC Layer): The host country tracks the physical reality of the atmosphere within its territory to meet its NDC.

- The Corporate Level: The company tracks its internal responsibility to balance its own footprint.

Because these two ledgers (National and Corporate) are never aggregated into a single global total, there is no mathematical “double counting.” This is the same logic we apply to Green Steel: the reduction is a physical fact for the country and a performance claim for the company. By adopting this nested model, we move climate accounting away from the “island” approach of the past and allow corporate capital to act as a mechanical engine for national progress. and toward a system that finally allows corporate capital to act as a mechanical engine for national progress.

The Simultaneous Effort for Exponential Growth

“Deep reductions must be finished before removals begin” is a fallacy. Both must happen in parallel to ensure durable CDR is viable by mid-century. CDR is NOT a replacement for the emission reductions. And it does not only balance hard to abate or unavoidable emissions, it is our only tool for helping the atmosphere to get rid of excess CO2.

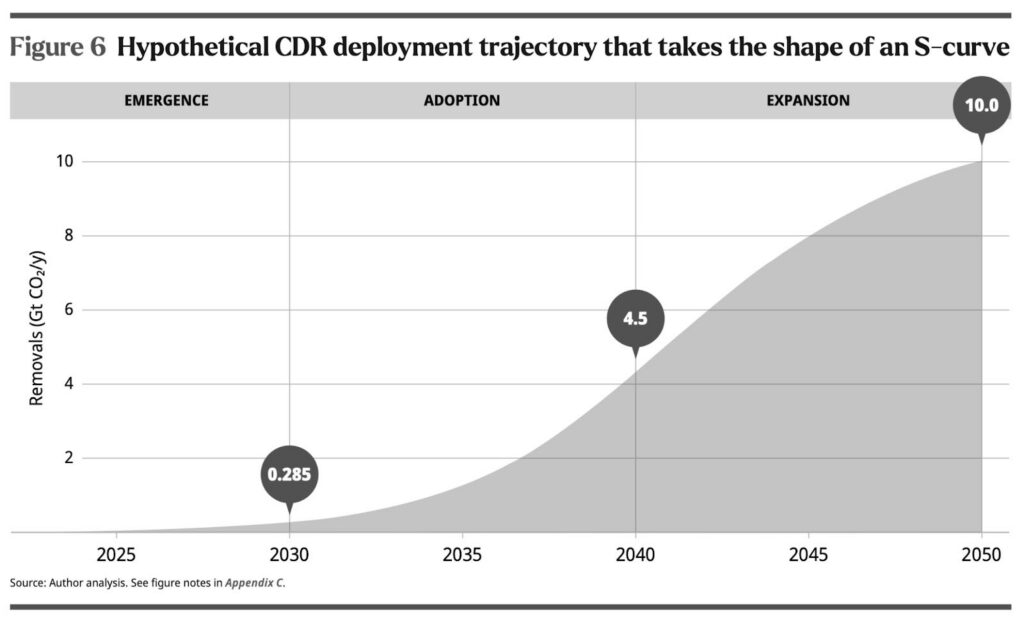

The S-Curve Logic

As the S-curve deployment trajectory from the RMI report prepared in collaboration with the Bezos Earth Fund “Scaling Technological Greenhouse Gas Removal: A Global Roadmap to 2050” shows, we are currently in the “Emergence” phase. This phase requires frictionless capital to move into the “Adoption” phase.

RMI: Scaling Technological Greenhouse Gas Removal: A Global Roadmap to 2050

- The Reality Check: We are currently at the base of the curve. Scaling requires an enabling environment.

- The 2050 Horizon: Exponential growth requires large-scale offtake agreements today. If we do not scale novel CDR technologies now, the infrastructure will not exist when it is most needed in the 2030s and 2040s.

- Parallel Tracks: Reductions and removals are a simultaneous requirement.

The CA Bottleneck While Corresponding Adjustments make perfect sense among countries, it transforms private offtake agreements into complex diplomatic negotiations. This added layer of sovereign bureaucracy is incompatible with the speed and volume required to move up the exponential curve.

A System for Action: Nested Responsibility

The final goal of 1.5°C or well below 2°C requires deep reductions and massive CDR. We need to replace complex legal adjustments with transparent, digital registries. These registries can clearly state: “This ton was removed, it belongs to the host country’s inventory, and it is matched by Company X’s financial claim.”

In this framework, “offsetting” remains a valid corporate performance metric. It is an internal calculation that drives private capital into national NDC projects. Here, co-claiming supports the host country’s goals while allowing companies to meet their internal net-zero milestones. The accounting stays within the NDC of the host country and is counted only once, nested in the global atmospheric carbon calculations.

We need a system that facilitates immediate action. A nested model can do that, allowing corporate finance to act as a mechanical engine for national progress today.

* Ghost tons: Carbon removals attributed solely to corporate claims through Corresponding Adjustments and excluded from the host country’s NDC accounting.